Credit Tenant Loan (CTL) Financing Continues to be an Attractive Way to Finance Resilient Single-Tenant Assets

As demand for single-tenant, triple-net commercial properties is on the rise, particularly for retail and industrial properties with tenants that provide or supply essential goods and services, CTL lending continues to be an attractive way to finance the acquisition and development of such properties.

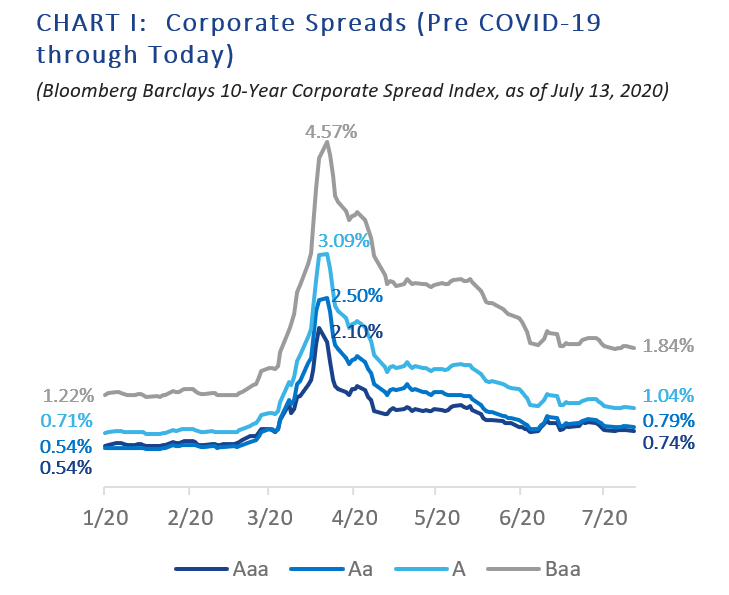

Despite COVID-related turbulence and recent volatility in the capital markets, CTL financing has proven to be an available and attractive way to finance single-tenant properties. While traditional lending sources are tightening underwriting guidelines and scaling back on leverage, CTL lenders (which are focused on credit rather than real estate fundamentals) continue to have a strong appetite for new loans, offering comparatively high leverage (up to 100% loan-to-value) for longer leases and relatively low interest rates, keeping in line with the compressed yield levels for corporate bonds (see Chart I).

With interest rates hovering around historic lows, now is the time to lock in long-term financing for properties that meet CTL criteria, namely existing or to-be-built single-tenant properties that have long-term leases with investment-grade tenants. In cases where lease terms have fewer than 15 years remaining, landlords should consider negotiating lease extensions or nudging tenants to exercise extension options to take advantage of the CTL debt currently available in the capital markets.

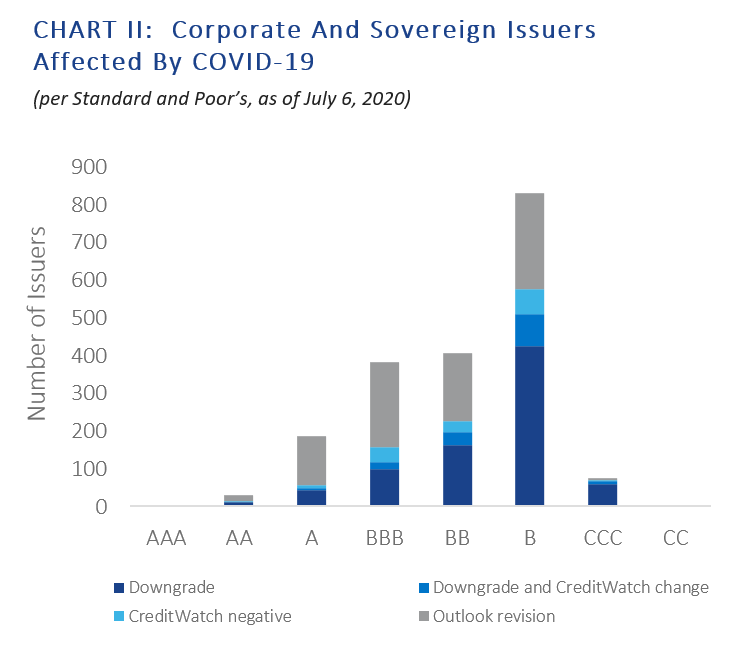

Although there appears to be a slight preference for A-rated tenants or better, there is still strong demand for CTLs with tenants across the investment-grade spectrum. Interestingly but perhaps not surprisingly, the vast majority of U.S. corporate companies that were investment grade before the pandemic maintained their investment-grade ratings by the end of the first quarter, according to a recent report by Standard & Poor’s. By and large, companies that were downgraded in the first quarter were already sub-investment grade to begin with (see Chart II).

In the first half of 2020, Waterway Capital closed CTL transactions for existing and to-be-built properties leased to tenants in the retail, industrial, health care, energy and municipal sectors. We are committed to helping our clients navigate the commercial real estate lending landscape in light of these extraordinary times.

Some information contained herein has been obtained form sources to be reliable but is not necessarily complete and its accuracy cannot be guaranteed. Any opinions expressed are subject to change without notice. It should not be assumed that any historical market performance information discussed herein will equal such future performance. This report is for information purposes only and should not be considered a solicitation to buy or sell any security. Waterway Capital LLC is a FINRA/SEC/MSRB member.